The Tax Cuts and Jobs Act represents the most significant overhaul of our tax laws in over 30 years. The act contains substantial changes to the taxation of businesses, individuals, multi-national companies, tax-exempt organizations and others.

Now, businesses large and small are considering the numerous changes that may affect them. The following outlines some key business-related provisions included in the act.

Corporate Tax Rate

The top corporate tax rate was reduced to 21 percent on January 1. The 21 percent rate is a “flat” tax that will apply regardless of a regular corporation’s taxable income; the progressive rate structure imposing a maximum 35 percent corporate tax rate is eliminated. Personal service corporations will also be subject to the 21 percent rate. For a fiscal year regular corporation, with a tax year ending in 2018, the new 21 percent rate will be “blended” with the rates in place prior to January 1, 2018. The act also repeals the corporate Alternative Minimum Tax for tax years beginning after December 31, 2017.

Pass-Through Income

For tax years beginning after December 31, 2017, the act generally allows a new deduction for individuals, trusts and estates of 20 percent of the domestic qualified business income generated by certain sole-proprietorships and pass-through entities (partnerships, S corporations and LLCs). Depending on taxable income, the deduction may be subject to a limit based on wages paid by the business or wages paid plus a capital amount, and certain service business activities may not qualify for the deduction. This deduction is slated to expire after 2025 like most other individual tax provisions in the act. In those instances where the full 20 percent deduction is available, the top federal tax rate for pass-through owners drops from 37 percent (the new top rate for individuals under the act) to 29.6 percent. In light of the tax rate changes, pass-through owners may want to re-evaluate the pros and cons of their current business structure.

Limitations on Net Interest Expense

Deductions for net interest expense are limited to the sum of (1) business interest income, (2) 30 percent of a business’s “adjusted taxable income,” and (3) floor plan financing interest for the tax year. Disallowed business interest expense is carried forward indefinitely. Adjusted taxable income is a specially defined term, and the definition changes after 2021 in a manner that will potentially make the limitation’s impact more significant. Businesses with average gross receipts of $25 million or less are exempt from this provision. In addition, certain businesses in the real estate and farming businesses can elect for the interest expense limitation to not apply.

Net Operating Loss Deductions

The net operating loss deduction for losses arising in tax years beginning after 2017 will be limited to 80 percent of taxable income. The act generally eliminates the carryback of net operating losses arising in years ending after 2017, but permits an indefinite carryforward.

Full Expensing of Business Assets

Qualifying business property, generally whether new or used, acquired and placed in service after September 27, 2017, and before January 1, 2023, will qualify for 100 percent expensing. Under the act, the expensing amount is phased down over four years: 80 percent for 2023, 60 percent for 2024, 40 percent for 2025 and 20 percent for 2026. For some types of property with long production periods and certain aircraft, these dates are extended one year. In addition, the act increases the section 179 expensing limits. It also expands the definition of section 179 property, for property placed in service after 2017, to include tangible personal property used in furnishing lodging (such as furniture and beds in hotels and apartments) and certain improvements to non-residential real property (such as roofs, HVAC property, fire and alarm systems and security systems).

Cash Method of Accounting for “Small” Businesses

The act increases the gross receipts threshold for regular corporations and partnerships with regular corporation partners (other than tax shelters) that can use the cash method of accounting to $25 million. In light of this change, affected taxpayers now using the accrual method of accounting may want to consider a change to the cash method. In addition, under the act, this increased threshold for gross receipts can simplify accounting for inventories and complying with the sometimes difficult uniform capitalization rules.

Excess Business Losses

Business losses in excess of business income of taxpayers other than regular corporations after 2017 (and before 2026) may be limited under the act. Net business losses in excess of $250,000 ($500,000 in a joint return) will not be deductible in the current year. Excess losses will be carried forward and treated as part of a taxpayer’s net operating loss in the subsequent year. This limitation could apply, for example, to losses from sole-proprietorships and pass-through entities (including farm losses).

Like-Kind Exchanges:

Like-kind exchanges (under section 1031) completed after 2017 are generally limited to exchanges of real property not primarily held for sale. An exception allows, in certain cases, the completion of deferred like-kind exchanges of personal property after 2017.

Excessive Compensation

Corporations treated as publicly held face stricter limitations on the deductibility of compensation paid to executive officers. The act revises and expands the definition of covered employees and eliminates the long-standing exception for performance-based compensation and commissions (subject to an exception for certain contracts in effect on November 2, 2017).

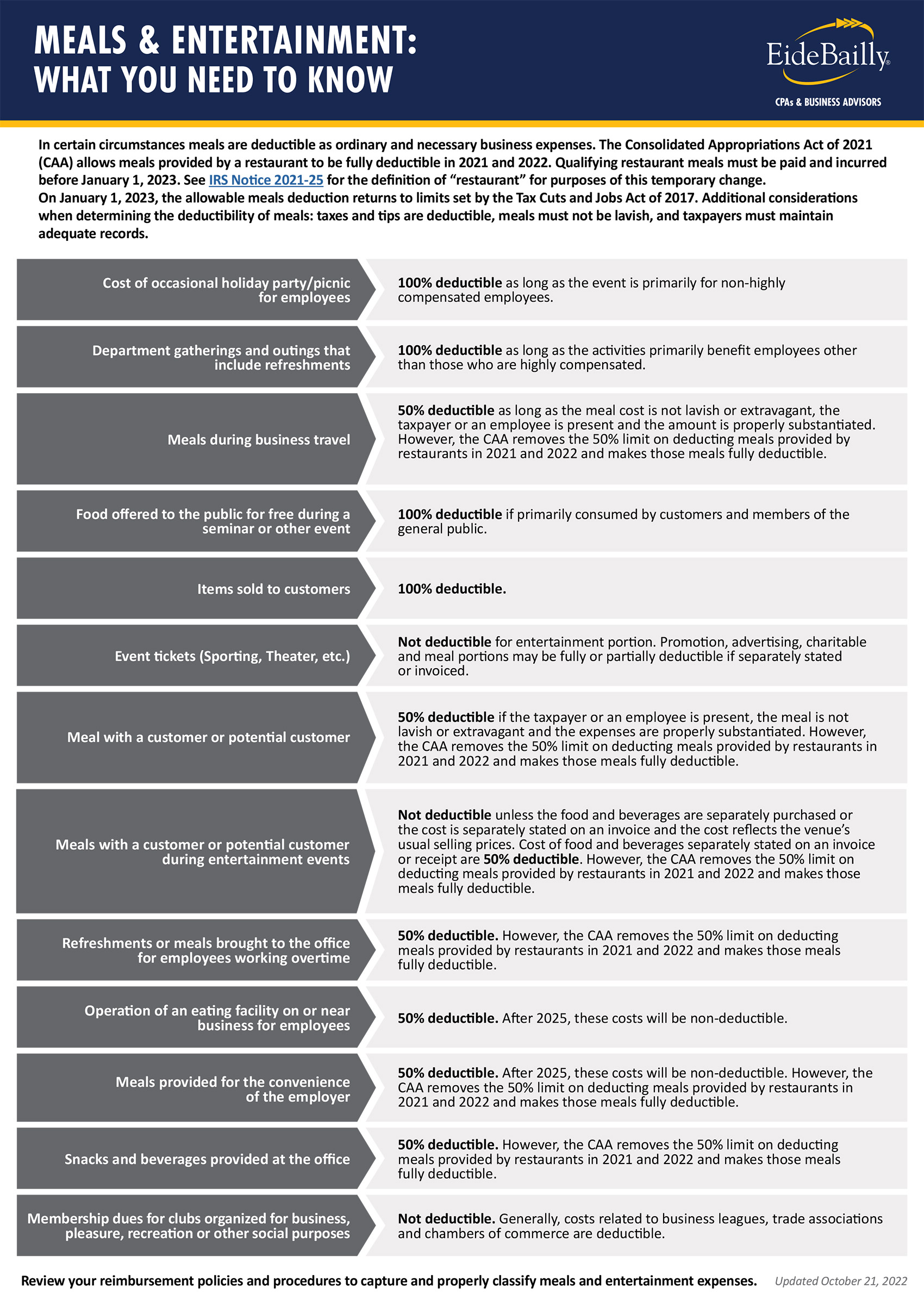

Meals and Entertainment Expenses

The act eliminates, after 2017, deductions for entertainment, amusement or recreation expenses, membership dues for clubs and expenses for facilities related to these items. While taxpayers will still be able to deduct 50 percent of meal expenses associated with operating their businesses—including meals during employee travel—the act extends the 50 percent deduction limit to employer-operated eating facilities through 2025. The act also disallows deductions for qualified transportation fringe benefits and certain expenses to provide commuting transportation for employees.

An Informed Approach

It is important to discuss your situation with your tax advisors and consider the best options moving forward to take advantage of available opportunities. For example:

- The lower tax rate for taxable income of regular corporations may make that form of business potentially more attractive and suggest modeling alternative business structures.

- Restructuring of pass-through businesses may reduce the impact of the limitations on the new 20 percent of qualified business income deduction.

- Accounting method changes may be available that accelerate deductions into higher tax rate years.

- The limitations on entertainment deductions may affect your employee reimbursement policies.

Ultimately, final decisions will depend on your particular facts and circumstances. Businesses have much to consider in the changing tax landscape.

We're Here to Help